Global growth is projected to decelerate sharply this year, to its third weakest pace in nearly three decades, overshadowed only by the 2009 and 2020 global recessions. This reflects synchronous policy tightening aimed at containing very high inflation, worsening financial conditions, and continued disruptions from the Russian Federation’s invasion of Ukraine.

Investment growth in emerging market and developing economies (EMDEs)

is expected to remain below its average rate of the past two decades. Further adverse shocks could push the global economy into yet another recession.

Small states are especially vulnerable to such shocks because of their reliance on external trade and financing, limited economic diversification, elevated debt, and susceptibility to natural disasters. Urgent global action is needed to mitigate the risks of global recession and debt distress in EMDEs.

Growth in low-income countries (LICs) is forecast to be 5.1 percent in 2023. Despite this year’s aggregate pickup, projections have been revised down for about two-thirds of LICs. Moreover, per capita income growth is expected to be a more subdued 2.2 percent in 2023. LICs are facing severe cost-of-living pressures, worsened by disruptions to global commodity markets—particularly for energy and staple cereals—following Russia’s invasion of Ukraine. Many more people have fallen into extreme poverty and food insecurity due to soaring food and fuel prices. The outlook for many LICs has deteriorated amid surging inflation, tightening financial conditions, fiscal and debt pressures, slowing activity in key trading partners, and heightened fragility. Risks to the baseline projections are mainly to the downside, including high inflation, resurgence of violence, debt distress in several countries, new COVID-19 outbreaks, and adverse weather events owing to climate change.

Given limited policy space, it is critical that national policy makers ensure that any fiscal support is focused on vulnerable groups, that inflation expectations remain well anchored, and that financial systems continue to be resilient. Policies are also needed to support a major increase in EMDE investment, including new financing from the international community and from the repurposing of existing spending, such as inefficient agricultural and fuel subsidies.

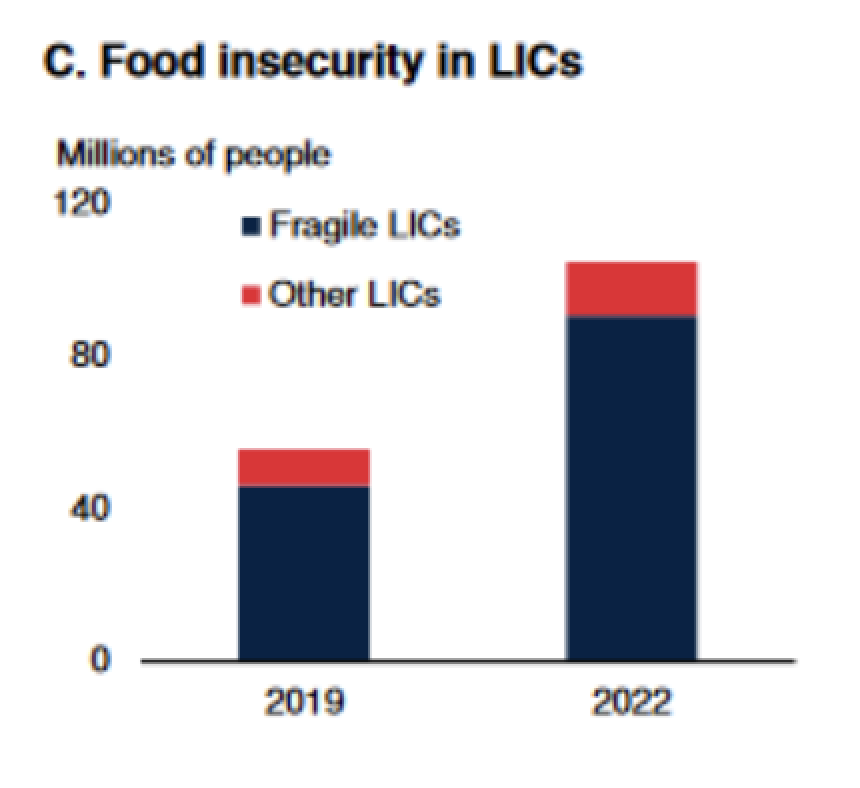

The international community needs to intensify its support to large numbers of displaced people and others affected by conflict or food insecurity, particularly in LICs (figure 1.2.C). In responding to food and energy shocks, governments need to avoid imposing export restrictions and instead attenuate the impact on the poor through support measures targeted at low-income groups. The international community also needs to reduce the risk of debt crises in EMDEs, including by supporting timely debt restructuring. Given the rising human and economic costs of more frequent climate-related disasters, particularly in small states, speedy action to foster the energy transition is critical for mitigating climate change.

Food insecurity remains a critical challenge in some EMDEs, reflecting the high number of food trade restrictions imposed last year, weather-related events, and the impact of the invasion of Ukraine and conflict elsewhere. As a result, about 220 million people are projected to face severe food insecurity in 2022, a number which could rise further if upward risks to food prices materialize.

Login (or register) to follow this conversation, and get a Public Profile to add a comment (see Help).

12 Jan 2023

Policy for Sustainable Food System Transformation through Agroecology Transition in Vietnam

Understanding farmers’ choices in climate-smart agriculture: adoption of agroecology principles and impacts on rural livelihoods in semi-arid Tanzania

Have crops already reached peak suitability: assessing global climatic suitability decreases for crop cultivation

Share this page